Premium

Net written premium for private carriers in 2025 remained at $41.6 billion, flat from 2024. Rates continue to decline overall, and written Bureau premium levels are expected to decrease by an average of 5% from 2025 to 2026 based on loss cost/rate changes in approved NCCI filings. Nevada is an outlier with a rate increase of 21.6%. This is mainly due to the growth of workers supporting the tourism sector, resulting in increased injury frequency in this jurisdiction. A significant rise in claim severity, as well as payroll cap limits growth in the exposure base, place additional upward pressure on loss costs in this state. Payroll increased by 4.8% in 2025, consisting of 0.5% from employment and 4.3% from wages. While wage growth was strong across many sectors, the largest employment gain was in the Health Care sector.

Economy

According to Stephen Cooper, Practice Leader & Senior Economist for NCCI, the U.S. economy entered 2025 on solid footing and continued to be resilient, having expanded significantly since the pandemic and outperforming many global peers. Consumer spending has remained strong and has been the backbone of the economy. While there are concerns about energy prices, inflation dynamics and other potential impacts of geopolitical events, forecasters continue to predict another resilient year of growth for 2026, led by productivity gains.

Inflation

Inflation remains a closely watched variable for Workers’ Comp, particularly on the medical side. NCCI’s Workers’ Compensation Weighted Medical Price Index (WCWMI – available on NCCI.com) indicates that medical inflation is around 1.8% as of March 2026. Should the more recent trend of price growth for medical equipment/supplies and inpatient services continue, NCCI would expect to see the WCWMI trend back up towards 2.5%.

Labor Market

Overall job growth in 2025 was very low at 0.5%. As the labor supply has softened, unemployment remains very low. As such, the labor market remains in balance as both supply and demand have cooled. Job separations have slowed as well. Reduced turnover and more tenured employees typically result in lower injury frequency. Payroll growth continues and there have been early signs of the labor market strengthening in 2026. While Construction jobs are rebounding, the predominant job growth is in the Health Care sector.

During a discussion on the impact of artificial intelligence on the labor market, Mr. Cooper stated that technological change impacting work has consistently caused some jobs to go away while new ones are created. It is his opinion that relational sectors (people to people) will likely account for a growing share of jobs in the future.

NCCI State of the Line Report

NCCI’s Chief Actuary, Donna Glenn, provided a detailed review of results, trends, and cost drivers in the Workers’ Comp industry. Here are selected highlights from her presentation:1

- WC Premium – The net written premium for private carriers remained at $41.6 billion for 2025. When including state fund data, the total net written premium was $45.6 billion.

- WC Net Combined Ratio – The 2025 private carrier calendar year (CY) combined ratio is 91%. The 2025 accident year (AY) combined ratio is 102%, but NCCI believes it will develop favorably over time and improve to 97% when all claims are settled and closed.

- Investment Results – The preliminary WC investment gain on insurance transactions ratio decreased slightly to 9% in 2025. It is noted that this is still below the WC long-term average of 11.3%.

- Pre-Tax Operating Gain – 2025 saw an 18‑point pre-tax operating gain (9% investment gain ratio and 9% underwriting gain). While this is the lowest value since 2016, it remains above the long-term average of 15.2%.

- Reserve Adequacy – NCCI estimates the year-end 2025 WC reserve position for private carriers to be a $14 billion redundancy. This is a further reduction from the $16 billion redundancy in 2024 but still a stark contrast to the $12 billion deficiency that existed in 2012. WC has been in a redundant reserve position since year‑end 2018.

- Claim Frequency – NCCI estimates WC lost-time claim frequency for AY 2025 is 2% lower than the previous year. This is a more moderate decrease in frequency compared to the long-term average annual change of ‑3.8%. NCCI expects the long-term downward trend in frequency to be likely to continue.

- Indemnity Severity – The average indemnity cost per claim for AY 2025 is estimated to be 4% higher (average cost $31.3K) than for AY 2024. The past three years saw larger-than-average increases in indemnity severity, primarily driven by increased wages.

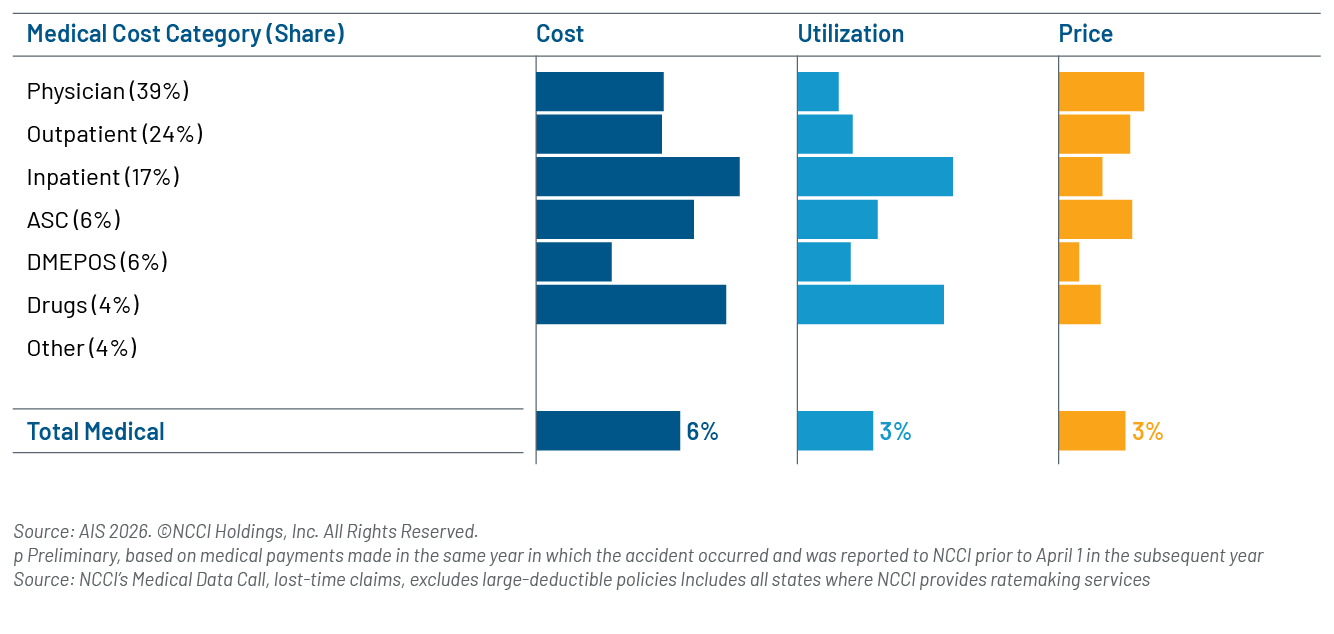

- Medical Severity – NCCI estimates the average medical lost-time claim severity for AY 2025 to also be about 4% higher (average cost $30.6K) than AY 2024. It’s noted that utilization, rather than price inflation alone, continues to influence medical cost trends.

Closing Thoughts

In her introductory remarks, Tracy Ryan, President & CEO of NCCI, set a forward looking tone by highlighting the overall strength of the Workers’ Compensation system while emphasizing the importance of staying alert to emerging changes. She believes the industry’s future will be shaped by three major forces:

- Shifting workforce dynamics (including where and how people work)

- Ongoing transformation within the broader healthcare system that directly affects claim outcomes and costs

- The rapid advancement of artificial intelligence, which is expanding capabilities across organizations

Ms. Ryan underscores that Workers’ Compensation must continually adapt to these trends.

Investments in safety, automation, data, and analytics have materially improved outcomes over the past decades, contributing to sustained profitability and system stability. However, we agree with Ms. Ryan that the industry’s continued success will depend on how well it proactively anticipates and evolves to properly respond to a changing environment. Gen Re is proud to support a healthy and resilient Workers’ Compensation marketplace and looks forward to working together to address future challenges and opportunities.

Endnote

- Full report is available at NCCI.com. 2025 data is preliminary.

This article was produced with permission from NCCI.