The systematic examination of nanomaterials and associated risks is of increasing importance to the insurance industry.

The insurance industry should aim to actively support nanotechnologies without losing sight of the risk potential from an underwriting perspective. In cooperation with The Innovation Society in St. Gallen, Switzerland, Gen Re has developed a risk monitoring system for engineered nanomaterials. The system is based on the collection of comprehensive scientific data and designed to support insurers in collecting and analysing potential nano risks in their portfolios.

Multifaceted materials with outstanding properties

Experts consider nanotechnologies1 and nanomaterials2 to be key technologies and key materials of the 21st century. All over the world, they are becoming ever more commonplace in industrial applications and consumer products. Many cosmetics, varnishes, plastics, electronic components and medical devices, construction materials, and even toner for printers (see box on p. 4) contain nanomaterials. Nanomaterials have the capacity to considerably improve material properties unlike to bulk materials.3 They are used, for example, as invisible filters in sunblock and as components in energy-efficient displays or lighting. Due to their extremely small size, nanomaterials possess a comparatively large specific surface, which means increased reactivity. A plethora of nanomaterials and applications are currently either being looked into or are almost ready for market launch.

Unknown long-term effects and regulatory gaps as risks

The insurance industry must face up to both the pleasant economic prospects associated with nanotechnologies and the potential risks emerging from them.

The risk profiles of nanomaterials are multilayered and complex. For some nanomaterials, the long-term effects on humans and the environment remain unknown. Some nanomaterials (such as certain carbon nanotubes, known as CNTs) may exhibit increased toxicity or even have carcinogenic effects. Yet current findings on the toxicity of nanomaterials are mainly based on animal or in vitro experiments. The impact of nanomaterials on human beings and the environment fundamentally depends on the type of material, physicochemical parameters, the form (free, suspended, bound) and exposure.

In many countries, nanomaterials are regulated within existing laws, just like conventional chemicals. Regulations adapted to the special characteristics of nanomaterials are not yet sufficiently established, and it may be a number of years until they are implemented. These conditions may lead to regulatory gaps. While some nano-specific regulations exist in the EU, no legally binding generic requirements or declaration obligations for nanomaterials have entered into force in the U.S.

Widespread use in consumer products and reputation risks

Nanomaterials are contained in many of consumer products. In general, consumers perceive nanotechnologies in a positive way and come into contact with a large number of nanomaterials (cosmetics, textiles, packaging, etc.), but the general population has very limited knowledge of nanotechnologies. However, they are critical of certain applications (such as, applications in food and cosmetics). Since many producers pursue reserved information policies and the declaration of nanomaterials is mostly not mandatory, manufacturers of nanoproducts face extensive reputation risks. Regardless of the actual toxicity of the materials in question, this could lead to losses in revenue. The problem is exacerbated by more rapid communication in social media and partly negative media coverage that focuses on the risks. In the course of “nano scandals” or other violent controversies, the reputation of nanotechnologies in general might be damaged.

Possible losses to liability insurance as a result of nanotechnologies

Based on the current state of the described developments, we affirm the potential of nanotechnologies to evolve into real risks for liability insurance policies. Given that nanotechnologies are commonplace around the world and can be found in numerous products and industries, many policyholders worldwide would be affected, which would considerably damage the insurance industry and entail consequences for almost all relevant areas:

- Public liability insurance

- Product liability insurance

- Product recall

- Employer’s liability insurance (workers’ compensation, employers’ liability)

A distinction between workplace and consumer exposure has to be made, since causality can be established more easily for workplace exposure.

Another important aspect for insurers is the unlimited defence costs granted within liability insurance policies. Claims based on alleged damages could increase substantially in the coming years. The complexity of nanotechnologies would lead to extensive and costly defence.

Nano risk monitoring with comprehensive risk focus

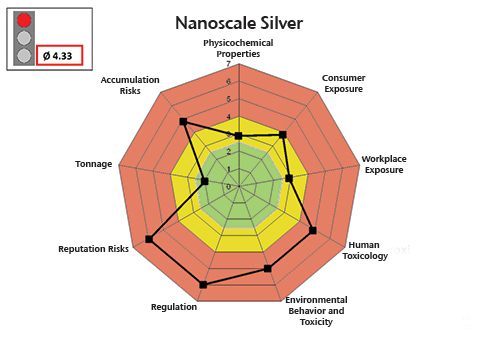

In order to enhance the insurability of companies manufacturing, processing or otherwise applying nanomaterials, Gen Re and The Innovation Society, St. Gallen have developed a risk monitoring system for engineered nanomaterials. The system is based on the collection of comprehensive scientific data and supports direct insurers in evaluating potential nano risks in their portfolios. In the process, the risk profiles of the most important nanomaterials are analysed and evaluated according to nine individual criteria, including toxicity, regulation, reputation and accumulation risks. The materials are categorised into risk classes and the risk profiles are visualised. The monitoring is updated according to client requirements and the latest scientific data is integrated into the risk profiles. Based on initial monitoring results, Gen Re advises the insurance industry to focus more heavily on nanomaterials.

Differentiated risk profiles and clear classification of nanomaterials

Nano monitoring is specifically designed to meet the requirements of insurers and takes into account the complex risks and opportunities associated with nanomaterials. Nanomaterials are not per se more dangerous than other materials. Nevertheless, insurers and policyholders have to consider that certain nanomaterials exhibit an increased risk potential. The risk profile of nanosilver is displayed in Figure 1.