- Property & Casualty

- Life & Health

- Knowledge Center

-

About Us

About Us OverviewCorporate Information

TOP

Gen Re is pleased to present this summary of key highlights from our 2019/2020 Medicare Supplement Market Survey. The full report covers Medicare Supplement results and market trends for 2019, capturing sales and in-force data, claim metrics, underwriting tools and practices, rate increase activity and compensation and distribution details. The comprehensive report is made available only to participating companies.

A total of 41 questionnaires were completed for this year’s survey, representing 85 companies with Medicare Supplement (Med Supp) business. Throughout this summary report, the percentage (or number) of companies refers to the 41 completed questionnaires. Depending on the type of question, not all companies were eligible to provide a response. To aid in your review, the number of respondents is displayed as “R=.” When reviewing the results please note that participants may vary from year to year.

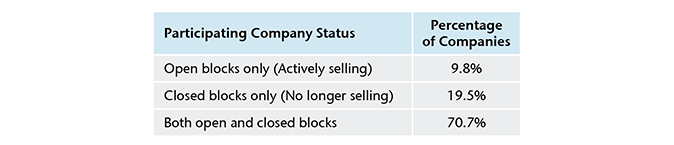

Participating companies were segmented by whether they have open and/or closed blocks of Med Supp business. “Open blocks” refers to blocks of business that accepted new applications in 2019. The majority of companies (70.7%) manage both open and closed blocks.

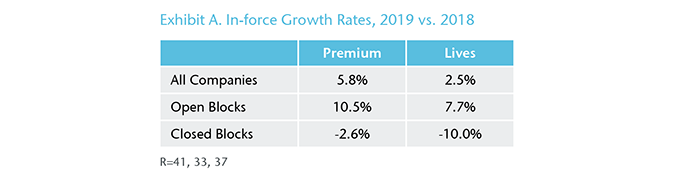

Participating companies reported $23.3 billion of Med Supp in-force premium for 2019, representing an increase of 5.8% over 2018. Open blocks account for 66.6% of the total premium or $15.5 million. Participants also reported 9.8 million covered lives, an increase of 2.5% over 2018. (Exhibit A)

In 2019, companies with open blocks reported nearly $1.8 billion of Med Supp sales premium, an increase of 21% over 2018. This result was mainly due to one company who reported that premium from new sales was heavily inflated in 2019 due to sunsetting of Medicare Cost plans. When excluding them from the growth calculation, new sales premium increases by 4.8% over 2018. Participants also reported covering more than one million lives, rising 12.8% over 2018. (Exhibit B)

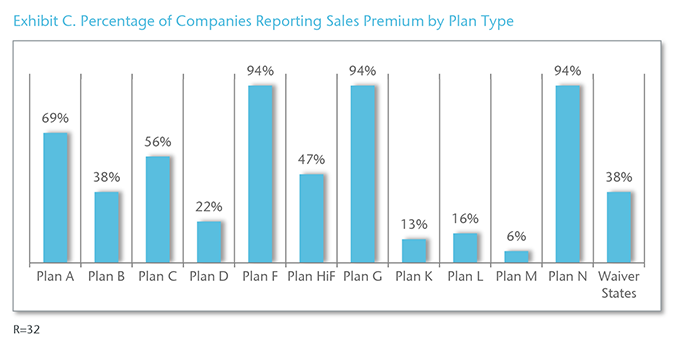

In 2019, 94% of the participating companies sold Plans F, G and N. Plans A and C were also popular with more than half of the participants selling those plans. (Exhibit C)

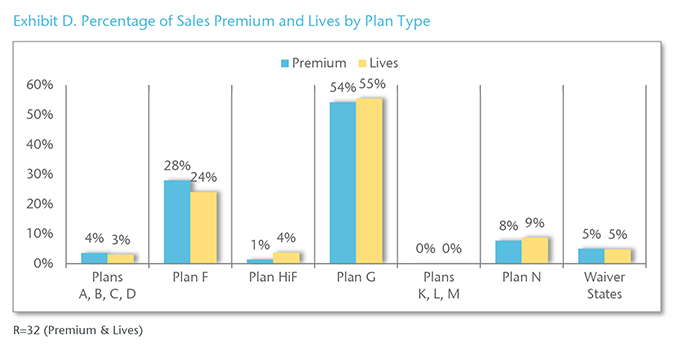

On a combined basis, Plans F and G accounted for 82.2% of the total sales premium and 79.5% of the total lives in 2019. (Exhibit D)

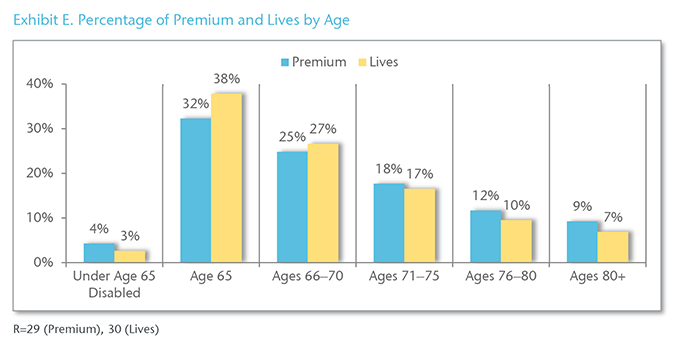

For 2019, 32% of new sales premium was attributed to policyholders who were age 65, while policyholders ages 76 and older represent 21% of new premium. (Exhibit E)

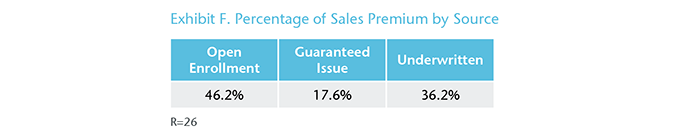

Overall, 46% of 2019 new sales premium could be attributed to open enrollment applications and 36% to underwritten applications. (Exhibit F)

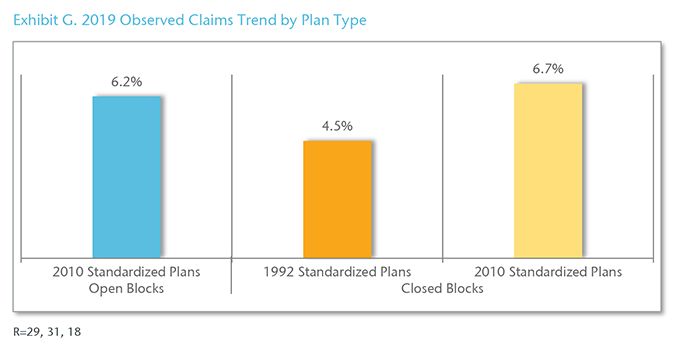

The observed claims trend for 2010 Standardized Plans averaged slightly higher (6.7%) for companies with closed blocks compared to 6.2% for companies with open blocks. (Exhibit G)

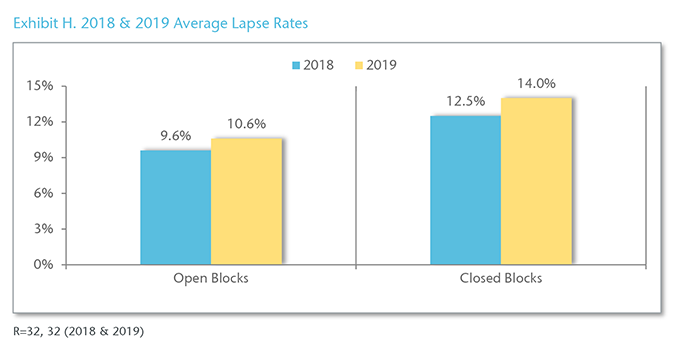

In 2019 lapse rates for open and closed blocks increased compared to 2018, averaging 10.6% and 14.0%, respectively. (Exhibit H)

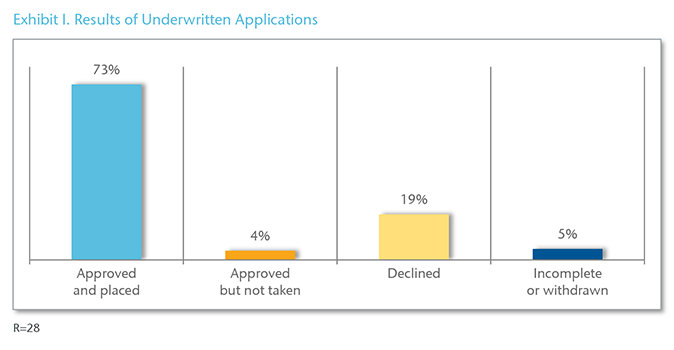

On average, 73% of underwritten applications were approved and placed, while 19% were declined. Of the 28 participating companies, 12 reported a decline rate greater than 20%. (Exhibit I)

In 2019, the average turnaround time on underwritten applications was 4.4 business days, ranging from one to 12 days. (Exhibit J) On average, companies keep an application open 37 days to obtain a requirement before closing it due to incomplete information.

For the purpose of this survey, an automated underwriting system was defined as a system to approve underwritten, web-based applications without human involvement. Of the 30 responding companies, six use an automated underwriting system and three plan to implement a system within the next 24 months.

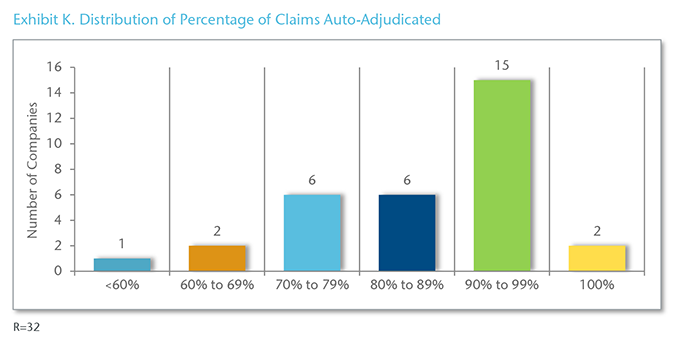

Overall, 91% of participating companies auto-adjudicate Med Supp claims. Of those companies, more than half (17) reported that 90% or more of their Med Supp claims are auto-adjudicated. (Exhibit K)

On average, 85.4% of claims are auto-adjudicated, with the percentages ranging from 20% to 100%. (Exhibit L)

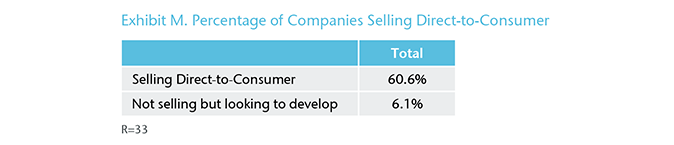

Direct-to-consumer was defined as selling a Medicare Supplement policy over the phone, online, via mail, or a combination of these methods without assistance from a traditional agent who is paid a traditional compensation. (Consumers can apply for coverage and go through the process without ever having to communicate with anyone.) About 61% of the participating companies currently sell direct-to-consumer, while 6% are looking to develop this capability. (Exhibit M)

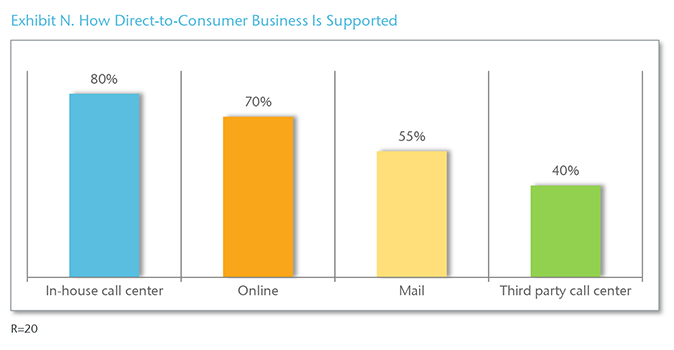

Most companies use an in-house call center as well as online support for their direct-to-consumer business. (Exhibit N) Eight companies use up to three methods to support their direct-to-consumer business and three companies use all four methods.

Download the PDF version for a list of participating companies.