- Property & Casualty

- Life & Health

- Knowledge Center

-

About Us

About Us OverviewCorporate Information

TOP

The seventh survey of Dread Disease insurance in Asia conducted by Gen Re examines the experience in China, Hong Kong, Singapore and Malaysia from the beginning of 2012 to the end of 2015.

For this survey, we decided to trim the number of markets covered from seven to four, as well as the number of companies, from 84 to 39. This was done in order to produce results more quickly as well as to focus on data quality. Although it may appear that the scope of the survey was reduced, the number of policies in-force at the end of the survey period was actually greater than ever before (110 million compared with 101 million in the previous survey) and a record 1.3 million claims were analysed.

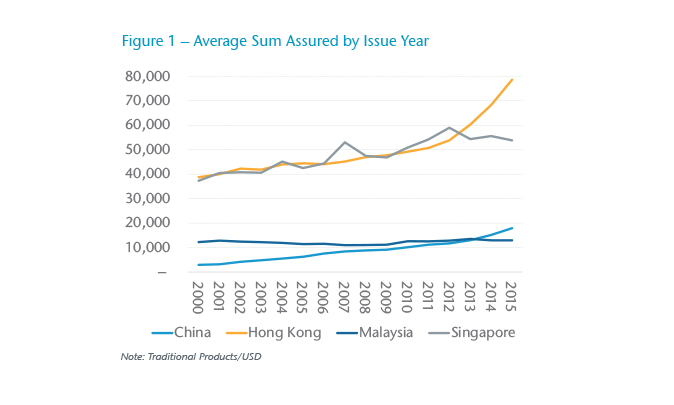

There has been a significant increase in the average sum assured in both Hong Kong and China (Figure 1). In Hong Kong the average sum assured from 2012 to 2015 for new business rose 46% to just under USD 79,000. This was largely as a result of increasing sales to wealthy mainland Chinese customers who came to Hong Kong to purchase large insurance policies there, instead from local vendors in mainland China. Although the average policy size in China (excluding Hong Kong) is much smaller, the increase over the same period was even larger at 53%. This continues the large growth in policy size since China was first included in the survey. In only 15 years, the average sum assured has grown around six-fold from about USD 3,000 in 2000 to almost USD 18,000 in 2015.

In contrast to Hong Kong and China, policy size in Malaysia and Singapore was largely flat over the survey period of 2012 to 2015.

In China, most of the new business now has a 90-day waiting period, compared with 180 days or even 365 days, which was standard in the early 2000s.

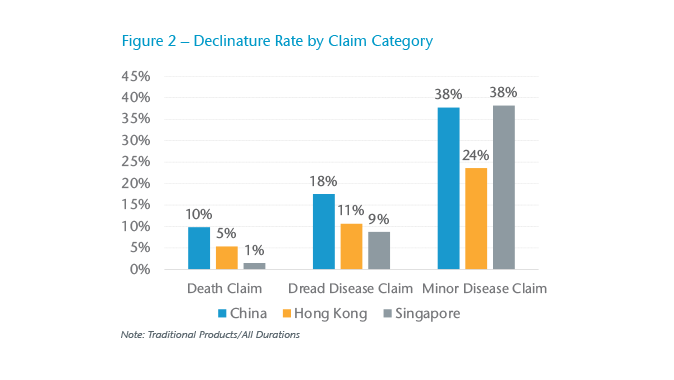

We found that “minor” disease claims (where the benefit payment is less than 50% of the full sum assured) have much higher declinature rates than those of “major” disease claims (Figure 2). The proportion of minor claims declined ranges from 38% in China and Singapore to 24% in Hong Kong. The corresponding “major” disease declinature rates are 18% (China), 9% (Singapore) and 11% (Hong Kong).

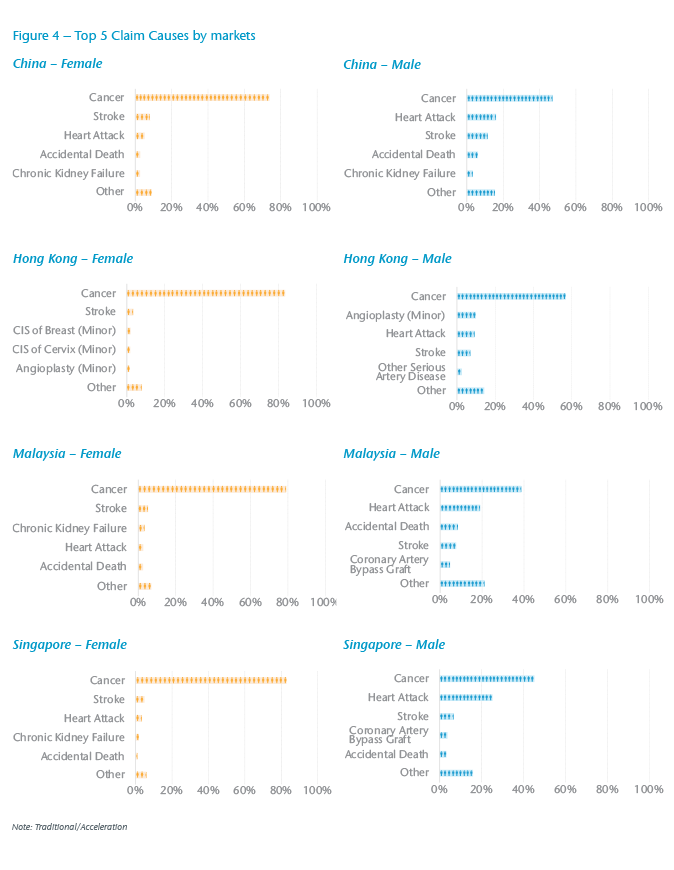

Cancer continues to be the single largest claim cause in every market, although the relative importance differs between males and females (Figure 4). For males it makes up from 39% of all claims (Malaysia) up to 57% (Hong Kong). For females, cancer is far and away the most significant claim cause, ranging from 74% in China to 83% in Hong Kong and Singapore. While cancer will continue to be the single largest claim cause in the future, we do expect other diseases to become relatively more important as portfolios age.

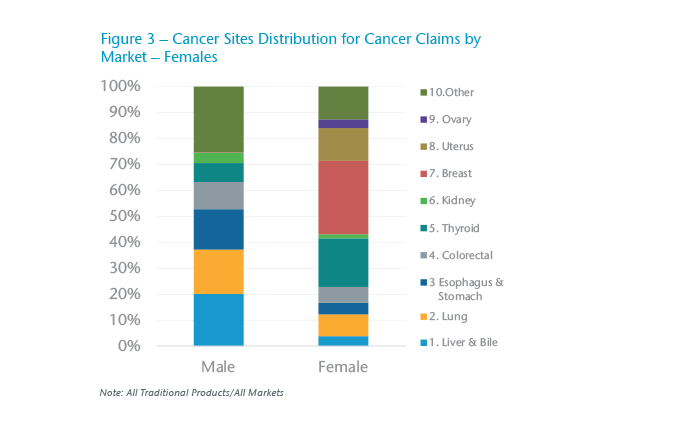

Breast cancer is the most common type of cancer for females in all four markets, ranging from 25% of all female cancer claims in China to 48% in Malaysia (Figure 3). In China thyroid cancer claims have risen rapidly and they now make up 20% of all female cancer claims. Hong Kong has also seen a rise in thyroid cancer claims but to a much lesser extent; they make up about 6% of all female cancers.

We also noticed a relatively high proportion of total claims from males coming from accidental death in both China (6.2%) and Malaysia (8.5%). One of the concerns with these high accidental death rates is that there may be anti-selection with people purchasing policies and intending to commit suicide. Although suicides in the first or second policy year are typically excluded from coverage, it can be difficult to prove that a death was indeed due to suicide. Therefore, we investigated accidental death causes that may well be as a result of suicide but difficult to prove as such. These included causes such as gas poisoning, falling from a height, drowning, etc. We combined these with confirmed suicides. The results show that in China for males, first year “suspected or confirmed” suicide claim rates are almost double the rates for later years. This leads to the conclusion that there is indeed a strong element of anti-selection. We did not observe this anti-selection in Malaysia, which also has a high accidental death rate, although the claims data was not always as detailed.

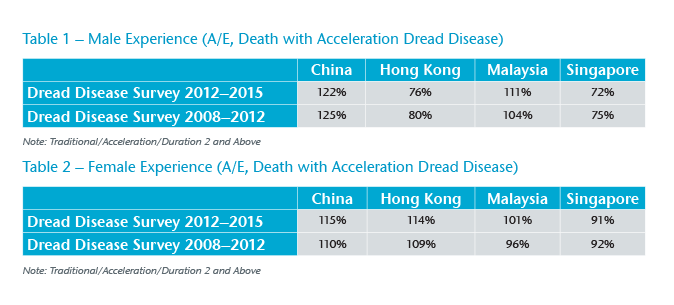

Overall, experience in China has continued to worsen. When China was first included in the 2000–2004 survey, it had the best experience of any market, but now it has the worst (Table 1 and Table 2). Note that the same “Expected” value is used in both surveys and is the same for all markets. The deteriorating experience has been driven by two factors. Firstly, Dread Disease is now a well-established product in China; it is likely that when Dread Disease was first introduced people were not always aware that they could claim. The second reason for the deterioration has been the large increase in breast cancer and especially thyroid cancer claims amongst females. These increases are driven by increased availability of health screening (meaning that cases are picked up earlier) and in the case of thyroid cancer, a weak definition. The rapid rise in thyroid cancer claims is of particular concern as there is no indication that the claims have peaked, meaning further deterioration is likely. There is also evidence of worsening thyroid cancer claims in Hong Kong, although the level is much lower than in China. In Malaysia and Singapore, we do not see any significant increase in thyroid cancer. However, there is still the possibility of worsening experience, although it is unlikely to deteriorate to the extent seen in China because of the stronger cancer definitions used in these markets.

In contrast with China, overall experience in Hong Kong, Malaysia and Singapore has been largely steady. In fact, Singapore shows a small but steadily improving long-term trend for both males and females, largely driven by reduced death claims.

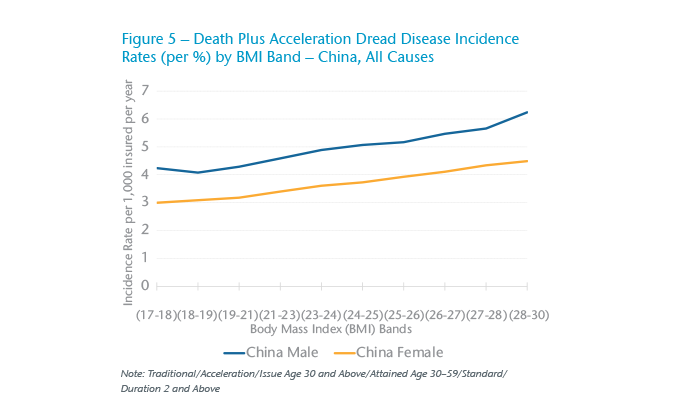

In China we obtained information about body mass index (BMI) for the first time. This showed that experience in the highest category (BMI 29 to under 31) was roughly 50% higher than the lowest category (BMI in the range 17 to under 19) (Figure 5). While this was expected, what was surprising was the fact that risk appeared to increase steadily and evenly across the range. Conventional wisdom is that risk only starts to increase once BMI exceeds 23 or 24 – but these results indicate a much steadier increase, starting at the lowest BMI category and progressing evenly to the highest. The worst experience for the higher BMIs comes from diseases such as heart attack, coronary artery bypass grafting (CABG), stroke and renal failure. Cancer rates increase very little with rising BMI.

For all markets, the results show that as sum assured increases, experience also improves for males. However, for females the situation is different. In Malaysia and Singapore, experience is relatively flat by sum assured band, while in China and Hong Kong it actually worsens.

In China we analysed experience by occupation category. There were two interesting results. Unemployed people, both male and female clearly had significantly worse experience than any other occupation. The second interesting finding was about people involved in the insurance, medical or legal fields. We suspected they might have poor experience since they might be in a better position to take advantage of Dread Disease insurance. Generally, this was not the case except for female medical practitioners whose experience ranked second worst amongst females, after the unemployed.

Finally, for China we were also able to analyse experience by region. This indicated big differences between the best and worst regions. For males, the North East provinces (Heilongjiang, Jilin, Liaoning and Inner Mongolia) had very poor experience, while Sichuan, Chongqing and Shanghai had good experience. The picture for females was similar, but with some notable differences: the experience for Shanghai was very poor for females, partly due to high breast cancer and thyroid cancer rates. When looking at individual diseases, there were even bigger discrepancies amongst the provinces. For example, heart attack rates for males in the North East provinces are around five times higher than the rates in Sichuan and Chongqing.

We hope that you enjoy reading our survey and find the information useful in your day-to-day work. Once again, we would like to thank the companies who participated for providing us with data as well as answering our questions. Without their tireless support, this survey would not have been possible.

We would also encourage you to give us any feedback or criticism about the survey as this will enable us to improve future issues of this work.