The product design has developed further in the German market (see below), but for the initial introduction of a new concept we suggest limiting the complexity.

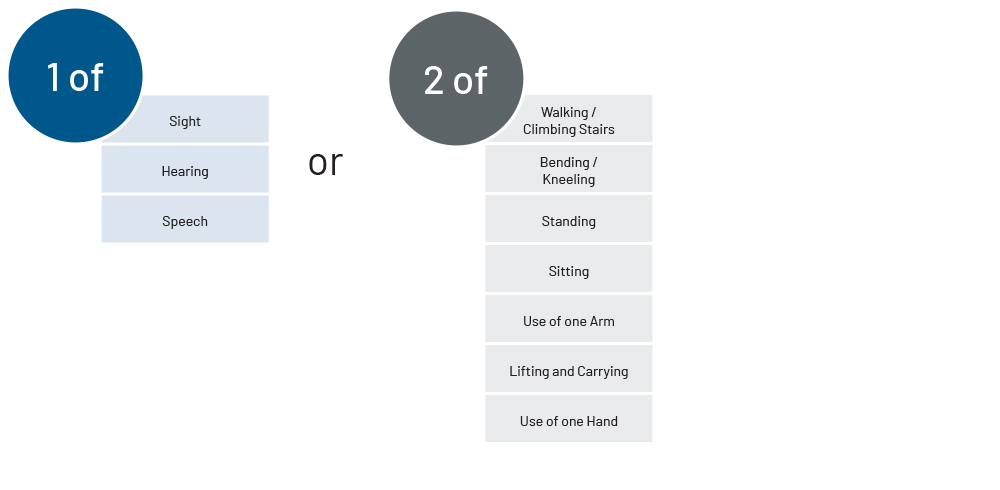

General Characteristics of the Benefit Trigger

The impairment should be caused by illness, injury or declining health and lead to measurable physical changes. The loss of an essential ability must be permanent and irreversible, and confirmed by a medical specialist. Deferment periods are recommended to exclude temporary illnesses, and to ensure benefits start after a minimum survival period of the life insured.

Underwriting

For a product design as described in this article, underwriting for EA cover leads to fewer ratings and/or exclusions compared to traditional DI and, often, to Critical Illness (CI). Fewer pre-existing conditions result in a loading or a declinature, meaning that the potential target group is larger, and it is possible to take out a policy even at an advanced age. Special focus is on pre-existing conditions of the locomotor system and impairments of the senses that may provoke anti-selective purchase of insurance cover. However, severe illnesses such as cancer, cardiovascular diseases, and diabetes must not be disregarded.

Questions on mental health should be included, even without an explicit mental trigger, as individuals with mental health issues have a higher risk of physical diseases. In fact, mental ill-health has a significant impact on a person’s physical health, sometimes less obvious (e.g. increased risk of heart attack or stroke, unfavourable lifestyle choices, etc.), sometimes more obvious (e.g. anorexia, substance abuse, etc.). Additionally, the elevated risk of suicide attempts associated with poor mental health may affect EA outcomes in cases where the attempt is not fatal.

Two occupational classes (white/blue collar) are recommended for simple versions or specified target groups. Only a few occupations are completely excluded from insurance coverage, such as explosives clearance specialists.

Disability can result from complications related to sports injuries and hobby accidents, ranging from short-term conditions such as sprains to long-term conditions such as those following a head injury. Information is therefore needed to assess participation levels in sports and hobbies.

Claims Management

Claims assessment for EA products is independent of the insured’s job activities at policy issue or just prior to disability. Additionally, mental disorders, which are difficult to assess, are less relevant since claims mainly arise from physical illnesses. Consequently, the claims process is typically faster for clients.

The examination usually starts by checking any non-disclosure. This is essential as this has been identified as an important issue by our claims assessors.

Unlike traditional DI, the impact of the medical diagnosis on the ability to work doesn’t need to be considered, but solely its impact on the loss of one or more of the covered essential abilities. The claims assessor should consider the symptoms or impairments that result from the diagnosis. The focus is on the claimant’s physical capabilities and limitations, rather than the diagnosis itself.

Standardised measurement sheets and, if available, discharge reports from rehabilitation centres are appropriate tools in claims assessment. Detailed claims assessment questionnaires can help medical practitioners examining the claimant understand the intent of the covered benefit. These questionnaires enhance the transparency of the claims assessment process and provide valuable insights that enable claims assessors to make an adequate claims decision.

Experience from Germany

EA products have become popular in Germany in recent years as a response to the limitations and expenses associated with traditional DI products. They are also a result of ever finer occupational classification in DI that increased the occupation-based premium spread. Now, most traditional disability carriers are offering them, and some are even selling more EA than DI policies. In addition to the number of providers on the market, the variety and complexity of products have also increased significantly (with expanded claim triggers and increasingly broad definitions requiring stricter underwriting).

The number of EAs offered in the market and other benefit triggers for annuity payments has roughly doubled over the past five years to more than 50. Sales are experiencing a high relative increase on still comparatively small absolute numbers.

Unlike with occupational DI, the trigger for benefits under EA insurance does not directly relate to the profession exercised, so the influence of the occupation on the premium is significantly lower: While roofers often pay many times the premium paid by a white-collar staff for occupational DI, the premium for EA insurance is often “only” 1.3 to 1.5 times higher – and for workers with less hazardous jobs, the premiums are in some cases no different from those paid by academics for EA insurance.

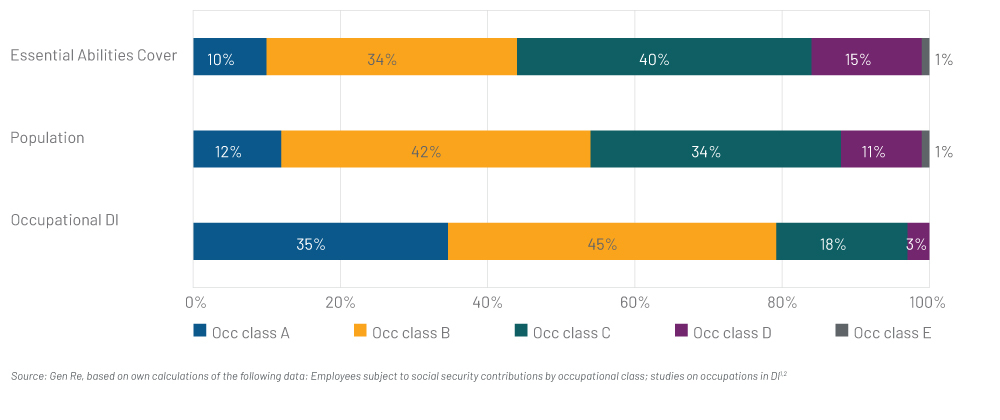

The resulting shift in the target group can be observed in new business: among all occupational DI policies, the lower-risk occupational classes A and B are significantly more common than their share of the population would suggest. Conversely, the share of higher-risk occupational classes C and D, as well as occupational class E – which includes occupations that are not covered by occupational DI as standard – is even higher than the population average. The EA cover thus successfully reaches the target group of physically active people and helps to ensure that broader sections of the population receive disability cover (Figure 1).

Figure 1 – Distribution of occupational classes in the German population and in new DI and EA business