- Property & Casualty

- Life & Health

- Knowledge Center

-

About Us

About Us OverviewCorporate Information

TOP

If I drive my vehicle half as much as last year and expect to continue doing so, does it make sense for me to pay just 15% less for my auto insurance? Does this mean my insurance company was taking advantage of me last year? Are they now? Considerations such as these demonstrate why interest in usage-based insurance (UBI) has been growing in 2020.

UBI relies on when, where, and how a vehicle is used, rather than MVR (motor vehicle records) and traditional driver characteristics like credit scores, marriage status and gender to determine premiums. This alternative type of vehicle insurance is not new. Progressive began experimenting with UBI more than 20 years ago1 by giving drivers dongle devices to keep in the vehicle to record driving behavior. Today, dongles are being replaced by applications on smartphones and a growing number of newer vehicles are already equipped with connectivity capability.

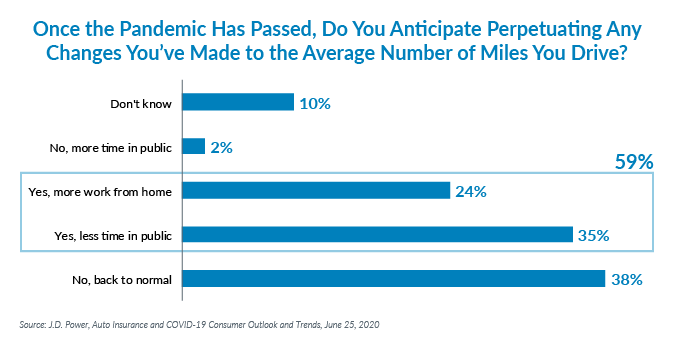

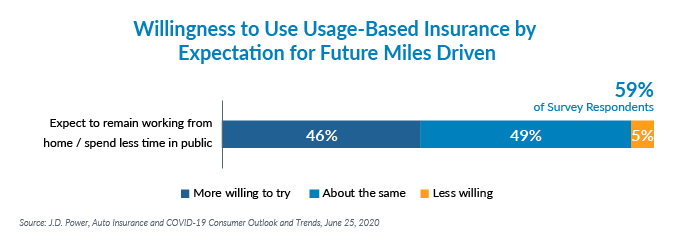

According to a June 2020 survey by J.D. Power, 59% of consumers expect to continue spending less time away from home, and 46% of those consumers are highly interested in UBI solutions.

Further, the auto insurance industry has close to a 20% satisfaction deficit versus pre-COVID.2 Satisfaction is a key driver of customer retention. And for the first time in its 21-year history, the J.D. Power U.S. Auto Insurance Study found that websites mattered more than a human agent for client satisfaction when interacting with auto insurers.3 Is this interest in UBI, and dissatisfaction with current insurance carriers and their procedures, enough to initiate a shift away from traditional auto insurance?

First, let’s consider the availability of such programs. Nine of the top 10 largest private passenger auto insurers have UBI programs in place.4 Alternatively, we recently conducted an informal survey among personal lines executives at 10 carriers with direct premiums written between $35M and $750M. Seven of the 10 carriers included in the survey do not currently have a UBI product.

Within our discussions we heard similar themes:

It’s understandable that companies of all sizes are hesitant to dive in. As mentioned earlier, Progressive first developed a usage-based product in the mid-1990s. It took about 15 years of testing before they released the first version of their current Snapshot product.5 Most companies don’t have that kind of time and money. Savings realized from developing better drivers and lowering acquisition expenses must outweigh the cost of researching and implementing the technology. Other challenges include a dearth of enthusiasm for the product within all ranks of the organization as well as their consumer and agency bases. State requirements for new rating plans vary, with some requiring statistical data and others raising privacy concerns. And UBI may not be a better alternative for drivers who work third shift hours or knowingly drive aggressively.

But as the technology continues to improve and younger, tech-savvy generations comprise more of the population, companies may find it worthwhile to rethink implementing a UBI program. Consider the following:

Several UBI platforms exist, such as The Floow, TrueMotion, Cambridge Mobile Telematics, and Arity. Costs associated with UBI technology will begin to decline as more insurtech companies develop such products. This will allow more carriers to adopt UBI products if desired. And it’s becoming increasingly common for car manufacturers to partner directly with insurers. On September 3, Ford Motor Company and Metromile announced a partnership “to provide Ford connected vehicle owners with personalized car insurance to be more affordable and fairer.”12

Technological advancements are increasingly impacting insurance companies and policyholders: Water leaks can be detected and stopped remotely; potential intruders can be seen and deterred; and vehicles can apply the brakes faster than the driver. Usage-Based Insurance is yet another quickly developing technology that may benefit insurers and policyholders. However, the benefits of a UBI product may not extend to all drivers. Furthermore, the implementation of a UBI platform may not pay off for every carrier. Regardless of an insurer’s position in the UBI development spectrum, it is prudent for carriers to be aware and educated about this growing form of auto insurance.