The COVID‑19 pandemic has caused all of us around the globe to rethink the paradigm around how we approach life. Many people have been asking novel and more complicated questions: How much socializing do I do in enclosed spaces? Should I work from home or in the office? Should I be saving more to protect my family or spending more to support local businesses? Should I move to a less expensive town at the cost of losing my current community? Is now the time to buy more insurance coverages or are they getting too expensive?

Market Results

Insurance purchasing behaviors have certainly changed during the pandemic. The Individual Life insurance market saw new sales premium drop in 2020 as agents’ abilities to get out and sell were hindered.1 Individual Disability insurance sales also suffered in 2020, with new sales premium down about 7%.2 In addition, potential buyers were understandably occupied with keeping their work and family lives going. But as the pandemic and its death toll continued to persist and climb, more consumers decided to purchase life insurance, with new sales premiums in 2021 growing by nearly 20%,3 while Individual Disability premium was flat in 2021 compared to 2020 according to Gen Re’s 2021 Disability Insurance Market Survey.

Impact of the Pandemic

As the reality of death became more front of mind for some individuals during the pandemic, so too did the vulnerability of a worker’s income, as millions of jobs were lost in early 2020. Disability insurance – or Income Protection insurance – fills a critical need in protecting an individual’s or a family’s income in the event of a disabling event. While not able to protect against the event of a job elimination, Disability insurance could replace a policyholder’s income if going to work becomes difficult due to a medical condition.

Some of the most common conditions that can result in a disability claim are back and musculoskeletal disorders, cancer, and some injuries.4 The COVID‑19 pandemic made it more possible to imagine being out of work due to complications from the illness or severe mental health issues stemming from social isolation or stress.

Yet…

An individual’s most important asset is often the income received from their job, generating millions of dollars over a lifetime. But a disabling condition removes that asset, and any replacement from Social Security Disability Income (SSDI in the U.S.) may only cover a small fraction of a disabled person’s income.

Unfortunately, there are over 50 million working adults in the U.S. that don’t have private Disability insurance coverage.5 According to a study done by Unum,6 a leading disability insurer, the most common reasons for forgoing Disability insurance are:

- “I’m healthy and don’t need it.”

- “I can’t afford it.”

- “I don’t see the value.”

The True Value of Disability Insurance

The reality is different than these perceptions. About 25% (1 in 4) of today’s 20‑year-olds can expect to be disabled before retirement.7 Injuries and cancer don’t seem to care what your cholesterol or glucose numbers are. Regarding affordability, the price point of a Disability insurance policy can be as little as about $1 a day for a 30‑year-old8 – you’re hard-pressed to find a cup of coffee as inexpensive as that today in the U.S.!

Finally, the value of Disability insurance is hard to overstate: Policies typically provide replacement of 50‑70% of an insured’s income, which allows most U.S. wage earners a higher income replacement ratio than SSDI alone (annual salaries of over $40,000 get less than 50% of income replaced by SSDI as of 2022). Losing one’s income for an unknown period of time inhibits the ability to pay bills on time, save money for an emergency fund, save enough money for retirement, make home improvements, and save for college. Given that a recent LIMRA study indicated the first three of these financial strains were in their list of top financial concerns impacted by COVID‑19,9 it shows that Disability insurance plays a vital role in maintaining financial wellness in a household.

Not only is Disability insurance a key tool to maintaining financial stability and wellness, but the U.S. Disability insurance market can provide valuable insurance coverage out of a position of strength.

Financial Stability of the Disability Insurance Market

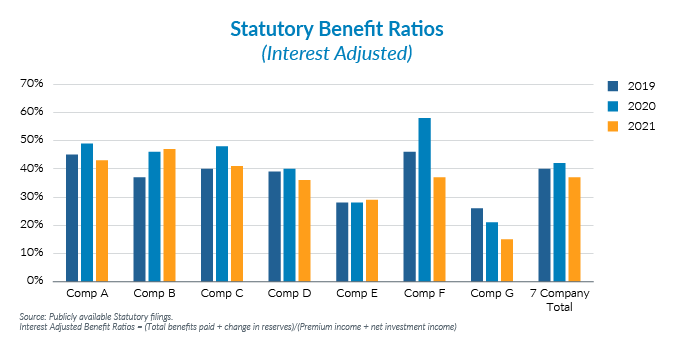

Statutory benefit ratios have been very stable throughout the COVID‑19 pandemic. This chart shows loss ratio results from seven of the top Individual Disability carriers, representing nearly $3 billion in annual premiums. The aggregation of these seven companies reveals that financial performance has been steady, with 2020 and 2021 benefit ratios averaging to the same level as 2019.