Effects on the Life/Health insurance market

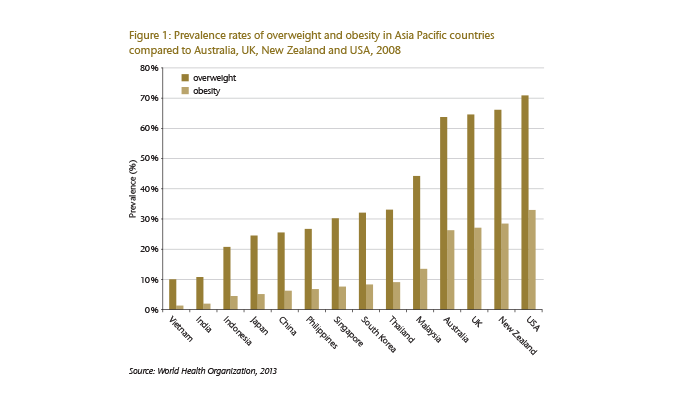

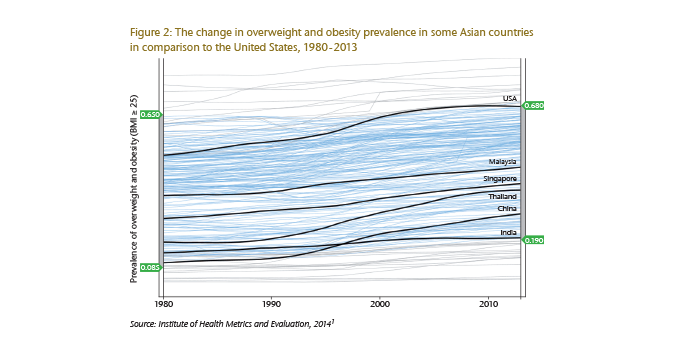

What we currently see in Asia is a divergence in nutritional status across geographical regions and socioeconomic status. This makes it difficult to generalize how increasing overweight and obesity rates will impact the Asian market. If the average BMI of the population increases, the additional mortality and morbidity risks may already be reflected in the baseline pricing. On the other hand, the long- term impact of overweight and obesity on mortality and morbidity may not be reflected in the past experience since the rising prevalence has been more pronounced only in recent years.

Mortality products

The effects of rising overweight and obesity prevalence on mortality products will be minimal in the long run, as the detrimental effects of obesity will be offset by better access to healthcare and improving medical technology.

Critical Illness products

The top three causes for CI claims in Asia are cancer, ischaemic heart disease and stroke,16 and the expectation is that the rise in obesity will directly influence the number of CI claims for obesity-affected risks. These include diabetes, heart disease, gallstones and certain cancers such as colorectal cancer, breast cancer in women, endometrial cancer, and cancers of the kidney, pancreas, liver and gallbladder.17

Health products

A prudent risk classification should ensure that overweight and obesity are appropriately rated for mortality and morbidity risk, or filtered out. The difficulty is in identifying individuals who will develop obesity in the future. Utilization of healthcare services by the overweight and obese is significantly higher – an obese patient spends US$ 2741 more a year for weight-related medical bills compared to a normal weight individual.18

Underwriting obesity in Asia

According to the build rating guidelines of Gen Re’s underwriting manual CLUE, a 35-year-old Asian will be accepted within the standard risk pool until he has a BMI of 29 and above. Underwriting for the Indian market is even more lenient as underwriters use the non-Asian BMI ratings, which only consider a BMI of 32 and above substandard risk.

A large proportion of Life and CI insurance applicants in Asia fall within BMI 25 to 30, a grey zone where the extra risks are small. Many of the people who are overweight or obese show unhealthy changes metabolically (e. g. raised blood pressure, raised cholesterol levels) and these indicators will be rated accordingly. This means that part of the extra morbidity and mortality risk is accounted for.

But what about the metabolically healthy overweight? The concept of being healthy and overweight has been debated over the past decade. In day-to-day underwriting, overweight individuals with no other ailments are rated as standard risks. However, recent studies suggest that overweight healthy individuals have an increased risk of cardiovascular events compared to normal weight healthy individuals.19

Despite the undisputable evidence that overweight and obesity increase the risk of multiple diseases, insurers in Asia continue to push the BMI cutoff for standard Life and CI ratings up. Nowadays, some insurers in Asia consider a BMI of 35 a standard risk, in an attempt to remain competitive. Fortunately, Asia’s obesity rates have yet to reach the extreme prevalence observed elsewhere and morbidly obese applicants are rare. With increasing media coverage of the “obesity pandemic” in conjunction with health initiatives, it is possible for Asia to curb the problem before it expands beyond control.

Download PDF version for Endnotes